How To Improve Your Credit In 10 Steps

What is Credit Repair?

According to Experian, credit repair is when a 3rd party company makes attempts to get information removed from your report. However, most of these companies are for-profit. Therefore, the FTC advises against this since there are many things you can do yourself for free.

Your credit score is made up of 5 different variables. 35% payment history, 30% amounts owed, 15% length of history, 10% new, and 10% diversity.

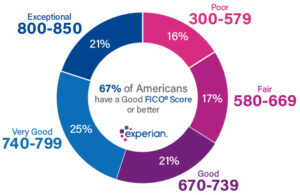

Your score ranges from 300 to 850 and in order to improve your score, it is important to pay attention to your FICO and VantageScore.

How to fix your credit

There are many things you can do to fix your score, however, it will not happen overnight. It is important to understand that fixing and maintaining your score is a long-term task that can take months, and in some cases, years.

It is also important to not get discouraged if you do not see drastic jumps. Your score constantly goes up and down, and one point here and there is fine so long as you stay in the “Good” or “Excellent” category.

Get your credit report

By making an account with Experian, you have access to view your report for free at any time. Experian also offers a FICO Score for free based on your report.

Dispute errors you find on your report

Mistakes happen to the best of us and sometimes you can have an error on your report and not even know it. After all, more than 1/3 of Americans found at least one error in their report. The good thing is, that it is very straightforward to get this error fixed. Experian offers an online portal to dispute these erroneous items on your report. There are a handful of common mistakes to look out for when viewing your report.

- Late payments

- High balances

- Default accounts

- Collections accounts

- Charge-offs

- Repossessions

- Foreclosures

- Bankruptcies

Make your payments on time

Making on-time payments is beneficial for rebuilding your score, but also crucial when it comes to maintaining a good score. Making your payments on time is incredibly important since it plays the largest role in your score, standing at a sturdy 35%. Enough late payments and your score could drop by up to 100 points. Late payments stay on your credit report for 7 years.

An easy and straightforward way to ensure you do not miss a payment is to set up autopay. If you are worried about over-drafting your account, we recommend setting up a budgeting system to help you better visualize and plan your spending.

Credit Utilization

Experian recommends keeping your total utilization below 30%. This ensures that you are not biting off more than you can chew. It also helps lenders see that you have controlled spending habits.

Keep old credit cards open

Keeping a long credit history is very important to your overall score, it makes up about 15% of your total. If you have a lot of accounts and want to close some, be sure not to close the one you have had the longest, as this will drastically affect your score.

Pay off the higher interest payment first

Depending on the type of debt, you should prioritize paying off the one with the highest interest rate first. This will help make sure that you are not paying more toward interest in the long run.

Increase your credit limit

Increasing your credit limit allows your utilization ratio to go down. This method is recommended to be used as a last resort or if you have an exceptionally bad score, as it gives you the opportunity to just dig yourself further into debt.

It is also important to understand credit cards for bad credit, will typically come at a higher APR and offer little to no extra benefits. So when looking to increase your limit, be sure it is with a card with the lowest APR you have, this will make sure you are getting the most bang for your buck.

Diversify your credit

The type of credit you have can also play a role in your overall profile. You want a diversified blend of investments to make up your financial portfolio. You also want a nice mix of saving goals and budgeting priorities to guide your spending habits.

There are two types of credit: revolving, and installment.

The installment type has a fixed end date with a series of payments due every month. Installment loans include mortgages, student loans, auto loans, and personal loans.

Revolving doesn’t have a specific end date or set balance. Instead of spacing out the balance equally over a certain length of time, a minimum payment is due each month. Credit cards are the most common type of revolving credit. A home equity line of credit (HELOC) is another type.

An ideal mix includes a blend of revolving and installment. An easy way to use revolving credit is to open a credit card—and pay your bill on time every month. Ideally, charge only what you can pay off every month to avoid interest.

If you don’t have an installment loan and only have credit cards, consider opening a small personal loan or other types of secured loan.

File for bankruptcy sooner than later

If bankruptcy is inevitable, Experian recommends not delaying the process. The sooner you can file for bankruptcy, the sooner you can begin rebuilding your score.

Keep in mind that your report changes over time. Meaning certain negative marks on your report will eventually fall off the report.

For a chapter 7 bankruptcy, this takes 10 years to fall off your credit report. Chapter 13 bankruptcy, collections accounts, and late payments fall off after 7 years. Hard inquiries on your account will be dropped after 2 years.

This should not be the only method you use to build your credit. Since this method is done independently, it is best for you to pair it with another item from this list.

Go to credit counseling

Credit counseling is a popular tool that individuals use when they feel they need to be better educated on how to deal with debt collectors. In addition to giving you the tools to work through debt settlements, they also assist with budgeting and general credit education. The ultimate goal of credit counseling is to eliminate debt.

What can I do?

Go Capital is an equipment financing company that can help you finance your equipment needs, even if you have low credit.

Contact Go Capital to get started today.

Need Funding for a Semi-Truck or Trailer?

Go Capital Can Help!

We specialize in helping trucker drivers with challenged credit. Get pre-approved today.

No Hard Inquiries – No Impact on Your Business or Personal Credit.